Prosperity Trading Terminal

A Bloomberg-style trading terminal and research platform for the IMC Prosperity algorithmic trading competition, supporting tick-by-tick market replay, strategy backtesting, order book visualization, execution simulation, and real-time performance analytics.

This project explores the design of a professional-grade trading terminal for algorithmic strategy research in the IMC Prosperity competition. The platform is built to replay historical market data tick by tick, visualize order book dynamics, test trading strategies, and analyze execution quality from a single interactive workspace.

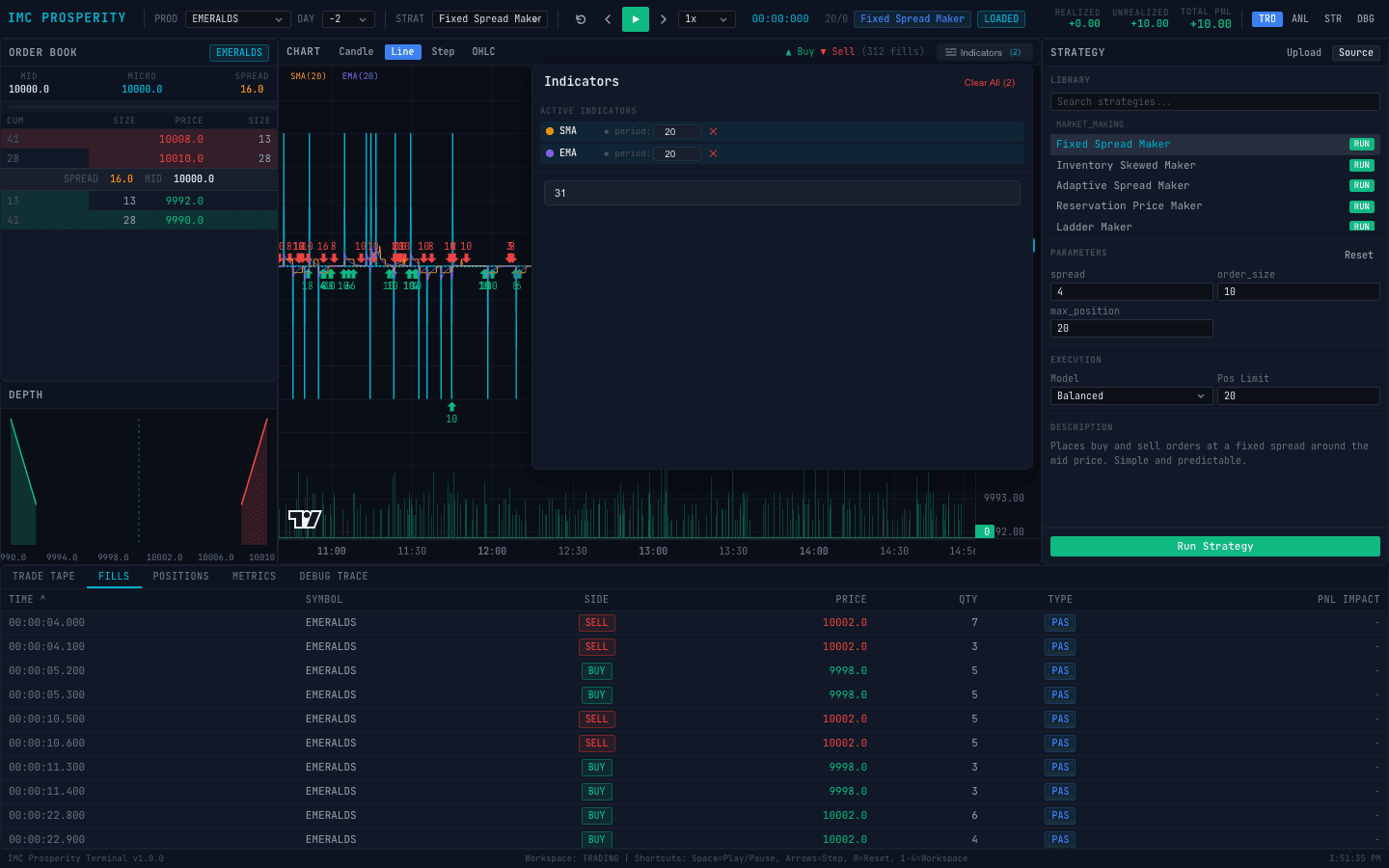

I developed a full-stack trading research system with a FastAPI backend and a React TypeScript frontend. The backend handles market data loading, CSV normalization, replay orchestration, strategy execution, fill simulation, backtesting, and persistence. The frontend provides a Bloomberg-style interface with resizable panels, keyboard-driven replay controls, real-time charts, strategy configuration, and live PnL tracking.

The core replay engine reconstructs historical order book states from IMC Prosperity price snapshots and trade prints. Users can select a product and trading day, step forward or backward through market events, adjust playback speed, and observe how the bid-ask ladder, depth chart, trade tape, candlestick chart, positions, fills, and PnL evolve over time.

The strategy engine supports both built-in and user-uploaded trading strategies. It includes market-making, mean-reversion, momentum, and microstructure-based strategies, along with a sandbox runner that executes custom Python strategy files through the IMC Prosperity Trader interface. This makes it possible to test strategy logic against realistic historical market states without manually wiring replay, orders, fills, and position accounting.

A major component of the project is the execution simulation layer. Because the competition data provides periodic order book snapshots rather than full Level 3 queue-level events, the platform implements multiple execution models. Conservative, balanced, and optimistic fill assumptions allow users to evaluate how sensitive a strategy is to passive fill uncertainty, book movement, and trade-print evidence.

The terminal also includes a rich analytics and visualization workflow. The frontend supports candlestick, line, step, and OHLC chart modes, fill markers, volume bars, technical overlays, and more than 200 configurable technical indicators. Backtest results are summarized through metrics such as total PnL, realized and unrealized PnL, Sharpe ratio, max drawdown, win rate, profit factor, trade count, and execution history.

To support live strategy debugging, the platform streams replay updates through WebSockets and exposes detailed per-tick traces. Users can inspect submitted orders, fills, positions, strategy notes, and running PnL at each market event. The terminal also provides multiple workspace layouts for trading, analysis, strategy development, and debugging, making it easier to move from high-level performance review to tick-level diagnosis.

Overall, Prosperity Trading Terminal demonstrates how market microstructure visualization, strategy backtesting, execution modeling, and full-stack engineering can be combined into a practical research environment for algorithmic trading. Instead of relying only on offline scripts, the system gives traders an interactive way to replay markets, understand strategy behavior, and diagnose performance under different execution assumptions.